Recently, Ancestry.com put indexed Tennessee tax lists from 1783 to 1895 online. Tax lists weren’t required to be saved, so these records are sporadic at best, but extremely valuable when they are still available.

http://search.ancestry.com/iexec/?htx=List&dbid=2883

I’ve been using tax lists for a long time, but since they are now becoming more widely available, I thought this might be a good time to talk about innovative ways to use tax lists to find “hidden” people of color. As we know, if you weren’t white, you were considered to be “of color,” generally to the 4th generation or in some timeframes in Virginia, if you had “one drop” of non-white blood. So Indian ancestors and mixed race people would have been found in the “people of color” category.

The purpose of tax lists was to determine the appropriate tax for people to pay – all people.

There were primarily two different categories of taxes, and lists. Sometimes these two types of tax lists were combined into one, but often not. Landowners could own multiple parcels in different sections of the county, meaning they would be listed more than once on a land tax list. But only one record of a poll tax would exist for any one person per county, per year.

The first type of tax was on land based either on acres or valuation.

But not everyone owned land, and heaven forbid, someone not pay taxes, so there were other types of taxes too. These lists were generally called poll tax lists but in some places were called personal property lists. There were columns of items and people to be taxed.

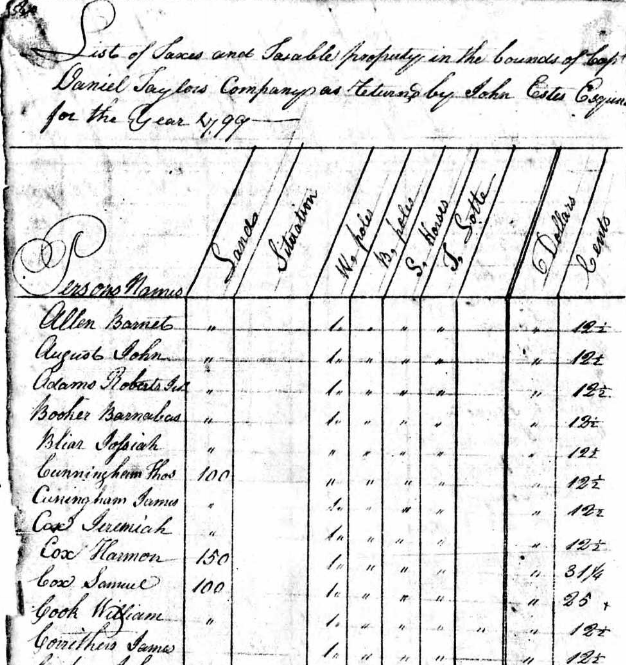

On the example below from 1799 in Grainger Co., Tn., you can see that John Estes, Esquire, took the tax list from within Daniel Taylor’s militia company. Categories were land, situation, which was used for exceptions, white polls, black polls, stud horses, town lotte, a blank column and then dollars and cents owed by the taxpayer.

White polls – were generally white males living in the household 16 years or older. The taxpayer, if white (unless exempt), would count as 1 and then any sons, other men, indentured servants, etc., would count too.

Black polls – depending on when and where, could be black males 12 and older or all blacks 12 and older. Obviously, this generally meant slaves but could also be free people of color who were counted on the land owners list if they did not pay individually.

Horses, cows, mules, etc. You’ll see various categories depending on the list location and year. Sometimes the horses are broken down to stud horses, which were money earners, and other horses. These often were indicators of relative wealth. I saw one list in Virginia where carriages and clocks were taxed.

Schools – in some regions during some time periods, there were special taxes collected for the school. The landowner whose land the school sat on was generally exempt from the tax.

Some people didn’t have to pay tax – if you were over a certain age – which varied from place to place and time to time but was generally 45-55 years of age, or if you were infirm and you petitioned the court to be excused from paying taxes, or if you were an ordained minister. On the list example, this would have been recorded in the situation column.

On later tax lists, there was more than one kind of tax, meaning both a state and a county tax.

Sometimes tax rates varied depending on your ethnicity. If you were a white person, your rates were, let’s say, 10 cents per acre but if you were “of color” they were a different rate, and generally not lower. Sometimes by comparing your ancestor’s taxes with those of known white neighbors, you can discern that they were considered “of color”. It goes without saying that the man who took the polls, or the tax list, in this case, John Estes, was white, so compare your ancestors rates with his. For example the amount of tax paid for a white poll or a black poll should be the same if both taxpayers were white, but if they are paying different amounts for the exact same thing, look for the reason why.

Families “of color” generally had to pay for all family members over the age of 12 (or 16) , including wives and children. In some locations, petitions were submitted to the legislatures to relieve free people of color of this extra tax burden. In some cases, men refused to pay poll tax on their mixed race wives and children and were taken to court for “concealing tithables.” In fact, concealing tithables is one hint that your ancestor may indeed have had a mixed race family.

Lastly, tax lists can be extremely useful sorting out various men of the same name. If someone owned land in 2 places within a county, especially if they were not adjacent and particularly if they were in 2 different districts, the same person can be on the tax list more than once if it’s a land based tax list. If it is not a land based list, meaning a personal property or poll tax list, then they would only be listed once. In some places, there were two lists, one for land and one for personal property. On those lists, by comparing them, you can tell if there were really 2 John Does or just one who owned land in 2 places. If there are actually 2 different John Does, their location will be somewhat identified by their tax list district, and their property of course would be located in that district, were you to find their deeds. By following the tax lists, so to speak, you should, hopefully, be able to tell men by the same name apart.

No one enjoys paying taxes, but for genealogists, these lists can be a goldmine if you know how to utilize the information.